Virginia Unemployment Refinancing Programs And AdviceWhenever VA interest rates drop due to Virginia unemployment, a refinancing frenzy naturally follows. Whether you're looking to trim your mortgage payments, eliminate credit-card debt or pay off your car loan, experts say you should fully understand all of the options available to you before deciding to refinance when you're unemployed. Virginia Unemployment Mortgage Consultants, a mortgage company recognized for educating consumers on the realities behind new home loans and refinancing, reveals seven common mistakes unemployed people make when refinancing.

1. Not saving enough to justify refinancing when you collect Virginia unemployment. It's best to decrease your rate by at least .75 percent to 1 percent. This will save you about $100 a month on a $150,000 mortgage.

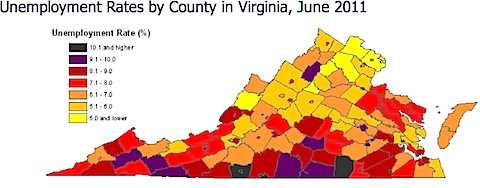

Virginia Unemployment

| 2. Not knowing your closing costs up front. By law, closing costs must be disclosed within three days of your Virginia unemployment eligibility application. However, there are different approaches to calculating them. Until the details of your loan are clear, the closing costs quoted to you are only estimates. Plan for the worst-case scenario.

3. Not fully understanding your reasons for refinancing. Besides reducing your interest rate, there are other legitimate reasons to refinance, such as debt consolidation, home improvements or major purchases. In some cases, you may be able to deduct your interest payments on your Virginia unemployment benefits. Always consult an accountant or tax attorney before making these types of decisions. 4. Not being aware of APR "teaser rates." Some mortgage brokers use annual percentage rates to get your attention, but it may actually end up costing you more. APRs often are derived by using a 30-year mortgage coupled with an accelerated payment plan. Make sure you know the actual interest rate you will be paying throughout your period of unemployment in Virginia.

Virginia Unemployment Eligibility

5. Not weighing the pros and cons of adjustable rate mortgages designed to the VA unemployed. ARMs can minimize your monthly payment, but not if additional refinancing occurs. In this case, they can cost more in the long run.

6. Not being aware of the service you should expect from a mortgage broker. The process of refinancing should be hassle-free and accomplished quickly. Ask your mortgage broker to provide details of its unemployment service plan and performance guarantees. 7. Not knowing to ask the mortgage broker about all available loan products, terms and rates. Subtle differences can save or cost you thousands of dollars. #virginia #unemployment |